Whether it’s part of a contentious divorce hearing or to assist a client in selling their business, a valuation is extremely important in determining the value of a business. Understanding risk factors is essential in determining how a business will be valued. Let’s consider what your business-owning clients need to know about company-specific risks and how they come into play when it’s time for a business valuation.

How Business Valuations Are Impacted by Risk

One of three approaches used to value a company is the income approach. Under this approach, it is assumed that the value of a company is equal to the present value of its future cash flows. To determine the present value of future cash flows, a valuator needs to determine an equity discount rate. The discount rate represents the expected rate of return that an investor requires to justify their investment, based on the amount of risk associated with the investment.

The two most common methods to calculate an equity discount rate include the Build-Up Method (BU) and the Modified Capital Asset Pricing Model (MCAPM). An important consideration when utilizing either the BUM or MCAPM is the determination of the specific risk associated with a company, also known as company-specific risk premium.

There are two components of risk: systematic risk and unsystematic risk. Systematic risk measures uncertainty unrelated to the company, like general economic conditions. Unsystematic risk measures the uncertainty of returns based on characteristics of the industry and the specific company. The company-specific risk is the risk premium associated with the level of unsystematic risk related to a company.

Methods of Determining Company-Specific Risk

There is no objective source of data or generally accepted calculation to quantify a company’s specific risk; it is left up to a valuator’s professional experience and judgment. In most cases, valuators will consider many different risk factors to determine the appropriate company-specific risk premium. These risk factors may include, but not be limited to, the following[1]:

- Economic risks

- Business risks

- Operating risks

- Financial risks

- Asset risks

- Product risks

- Market risks

- Technological risks

- Regulatory risks

- Legal risks

When applying the income approach, the valuator must consider these risks in relation to the market-derived rates already determined. For example, if the industry the subject company operates in has low barriers of entry, that risk may already be taken into consideration when examining guideline companies for an industry-risk premium.

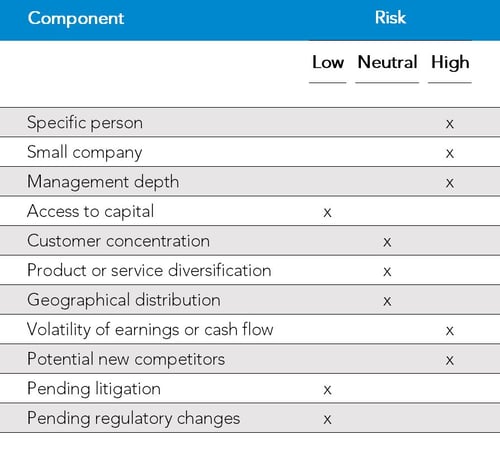

One method, shown below, that a valuator might use to determine the company-specific risk premium is a chart to analyze the different components of company-specific risk.

In this example, the valuator analyzed 11 different unsystematic risk components commonly used to determine company-specific risk. Instead of assigning a value or percentage to each component, the valuator used low, neutral and high impacts on risk to determine whether the factor would increase or decrease the discount rate, and how important each of these factors is.

An example of one of these components could be a single person in management, who makes all company decisions. The valuator might assess both the specific person risk and management depth risk to be high. If the company has a seasoned and sizable management group, specific person risk and management depth might both be assessed as low. After going through these factors, a valuator must still use their professional judgment to convert these factors into a risk premium.

In rare cases, company-specific risk can be negative, but generally it ranges from 0% - 10%.

Reducing the Company-Specific Risk Premium

In general, a higher company-specific risk premium results in a higher cost of capital, which results in a lower value for the business. The lower the company-specific risk premium, the lower the cost of capital and the higher the value of the business.

For a business owner considering a sale, reducing risks can result in maximizing value. While some risks cannot be readily changed, they may need more thought and consideration from a potential buyer. For example, the potential of new competitors is always a risk, and not one that can be easily mitigated, even for very niche businesses. A good way to defend against these risks is offsetting them by reducing other risks, like specific person risk or management depth.

Bottom Line

When determining a company-specific risk premium, it is important to take into consideration what the total rate of return will be, given the risks of the benefit stream being discounted. The final equity discount rate has to make sense and the company-specific risk premium is just one component of that final discount rate.

Need Help?

Contact us here or call 800.899.4623 for help.

[1] Gary Trugman, Understanding Business Valuation, 6th ed., 491-492