Determining a couple’s income is one of the most critical financial issues in a divorce case. Reviewing the couple’s Form 1040, to start, can help paint a picture of their financial position and lifestyle.

Divorce attorneys who know where to look for key information on tax returns can gain an edge over their opponents. Everyone is required to disclose certain information in their tax returns, including total income, wages and alimony received. These numbers can serve as compelling evidence when making a case for identifying and dividing marital assets, proving the existence of hidden assets and determining income for support purposes.

Let’s consider what an individual’s personal tax return can reveal, and where to look.

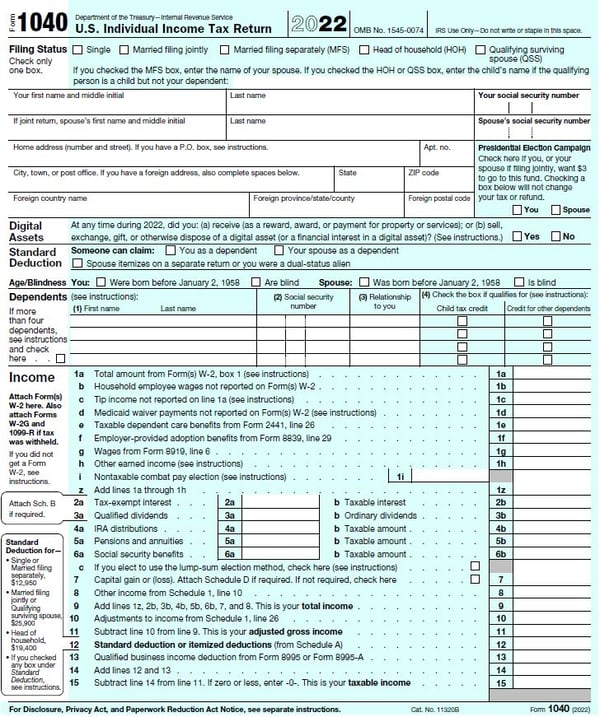

IRS Form 1040, U.S. Individual Tax Return

Form 1040 is where personal income is reported. The first page of Form 1040 provides a good overview of income, but only scratches the surface of what makes up the individual’s total income. W-2 wages on Line 1a is the first thing you see when looking at Form 1040. (W-2 wages should be confirmed by obtaining all W-2s from the client.)

While Form 1040 is the logical place to start when reviewing an individual’s tax return, it doesn’t necessarily reflect their full earnings. Form 1040 does not show 401(k) plan contributions, stock options, restricted stock vesting or employer loan forgiveness. You can find this information on the W-2.

The first common place to see non-W-2 income begins on Line 2a of Form 1040.

Form 1040

Form 1040

Identifying Investments Held In the Marital Estate

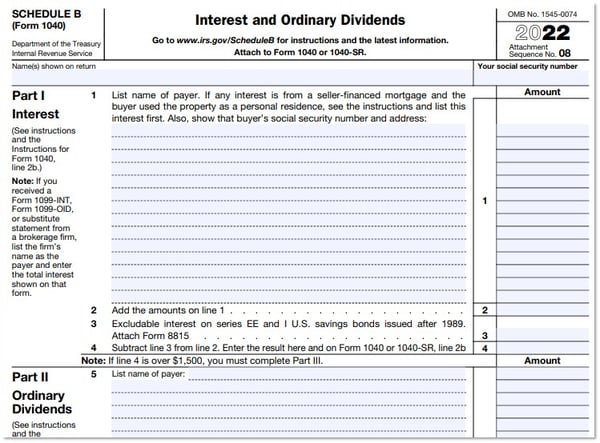

Let’s move on to Schedule B of Form 1040. Schedule B shows interest and dividend income from bank accounts, brokerage accounts and dividend income from S corporations, partnerships and other pass-through entities. This information allows you to identify the investments held in the marital estate.

Schedule B

Schedule B

Another important thing that Schedule B can reveal is the approximate total value of your client’s investments. For example, if Mr. and Mrs. Smith have $15,000 of taxable and nontaxable dividends, you can estimate that their investments total about $750,000 in assets such as stocks, bonds and cash in the bank. This calculation is based on an average dividend yield of 2% ($15,000 divided by 2% equals $750,000).

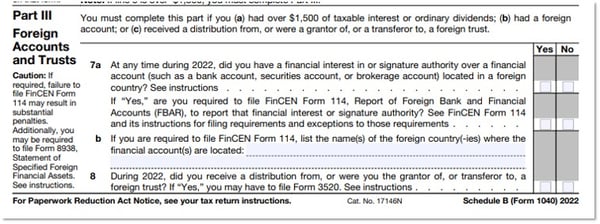

In addition, the bottom of Schedule B requires the taxpayer to indicate if they had a financial interest in or signature authority over a foreign account or trust. This might be helpful in identifying potential hidden assets.

Schedule B

Schedule B

Identifying Other Assets Based On Capital Gains and Losses

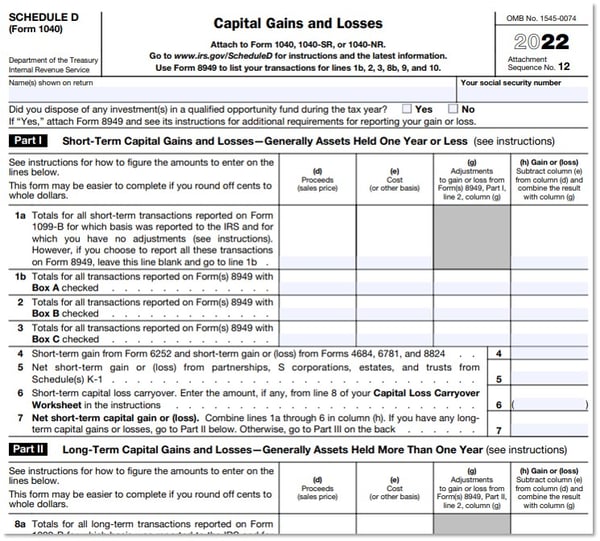

Capital gains and losses are reported on Line 7 of Form 1040. Schedule D is used to detail the sale or exchange of a capital asset that is not reported on another form or schedule. Schedule D shows both short-term and long-term capital gains or losses. Capital assets consist of all personal property, including a home, car or digital assets, to name a few.

Schedule D will not provide information about current values of investment portfolios or other capital assets, but it will tell you if a taxpayer recently sold stock and how much. It also may help identify investment accounts to ensure that you have captured all marital assets.

Schedule D

Schedule D

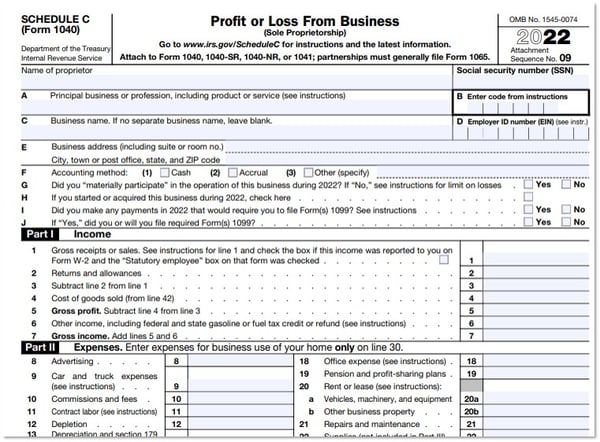

Identifying Income From a Business (Sole Proprietorship)

If income is being generated from a sole proprietor, Schedule C is where it is reported. On Schedule C, you’ll find the business name and address, primary product, service or profession, and a detailed reporting of income and expenses. Some items reported as business expenses can be related to personal use of business property, such as automobile and truck expenses and health insurance.

Schedule C

Schedule C

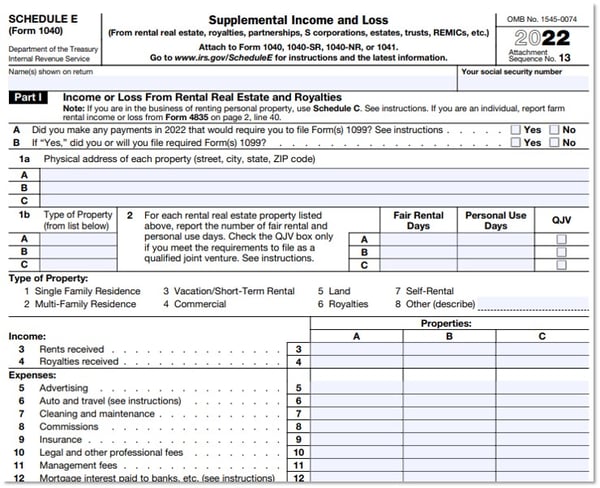

Looking for Supplemental Income and Losses

Supplemental income and losses are reported on Schedule E. This includes income from rental real estate, royalties, partnerships, S corporations, estates, trusts and REMICs (real estate mortgage investment conduit).

Part I of Schedule E shows income or loss from rental real estate and royalties. Here you will find the address and type of property being rented, and a profit and loss statement that shows whether the property is generating cash flow.

Schedule E

Schedule E

The second page of Schedule E includes information about the taxpayer’s business ownership. An analysis of Schedule E and its supporting statements, along with any applicable Form K-1s, can help you understand the taxpayer’s investment details. Schedule E and accompanying documents show the name and type of the business entities, details of the spouse’s ownership percentage, any change in ownership, and whether the investment is of an “active” or “passive” nature.

Digital Assets

As more taxpayers invest in digital assets such as cryptocurrency, stablecoins or non-fungible tokens (NFTs), it is increasingly important to identify these assets when preparing an asset schedule for the marital estate. On the Form 1040, there is a required checkbox for a taxpayer to identify whether they received or sold digital assets. If this box is checked “Yes,” it would indicate the presence of digital assets. If the box is checked “No,” it does not necessarily mean there are no digital assets held by the taxpayer. It just means that they did not receive or sell any of these assets during the tax year.

![]() Form 1040

Form 1040

Need Help?

Contact us here or call 800.899.4623 for help.